As a business owner or payroll manager, withholding federal income tax from employee paychecks is one of your core responsibilities. Get it wrong, and you risk IRS penalties, unhappy employees, or even personal liability. Fortunately, the process is straightforward once you understand the key steps.

Step 1: Have Employees Complete Form W-4

The foundation of accurate withholding is the employee’s Form W-4 (Employee’s Withholding Certificate). New hires must fill this out on their first day, and existing employees can update it anytime (e.g., after marriage, childbirth, or a second job).

The current W-4 (redesigned in 2020) no longer uses “allowances.” Instead, it has five steps:

- Step 1: Personal information and filing status (single, married filing jointly, head of household).

- Steps 2–4: Adjustments for multiple jobs, dependents, other income, or extra withholding.

- Step 5: Signature.

Encourage employees to use the IRS’s online Tax Withholding Estimator tool for accuracy—it helps avoid under- or over-withholding.Step 2: Determine Withholding AmountUse the employee’s W-4 data along with IRS-published methods:

- Percentage Method: Ideal for automated payroll software.

The IRS provides tables in Publication 15-T (updated annually) based on filing status, pay period (weekly, bi-weekly, etc.), and gross wages.

Example: A single employee paid $2,000 bi-weekly with no adjustments might have $218 withheld (2025 tables). - Wage Bracket Method: Simpler for manual calculations.

These tables (also in Pub 15-T) let you look up withholding directly by pay range and filing status.

Both methods account for:

- Gross wages (before pre-tax deductions like 401(k) or health premiums).

- Pay frequency.

- Any extra withholding requested in Step 4(c) of the W-4.

Step 3: Handle Special Situations

- Non-resident aliens: Add a fixed amount to wages before applying tables (see IRS Notice 1392).

- Supplemental wages (bonuses, commissions): Withhold a flat 22% (or 37% if over $1 million), or aggregate with regular wages.

- Exempt employees: Only if they claim “EXEMPT” on W-4 and meet strict criteria (no tax liability last year, expect none this year).

Step 4: Deposit and ReportWithheld federal income tax (plus FICA) must be deposited on the same schedule as FICA—monthly or semi-weekly. Report quarterly on Form 941.Common Mistakes to Avoid

- Using an outdated W-4 (pre-2020 forms are still valid but less accurate).

- Forgetting to adjust for mid-year W-4 changes.

- Ignoring state income tax withholding (separate rules apply in most states).

Payroll software like Gusto, ADP, or QuickBooks automates most of this, reducing errors significantly. Staying compliant protects your business and ensures employees get accurate refunds (or avoid surprises) at tax time.

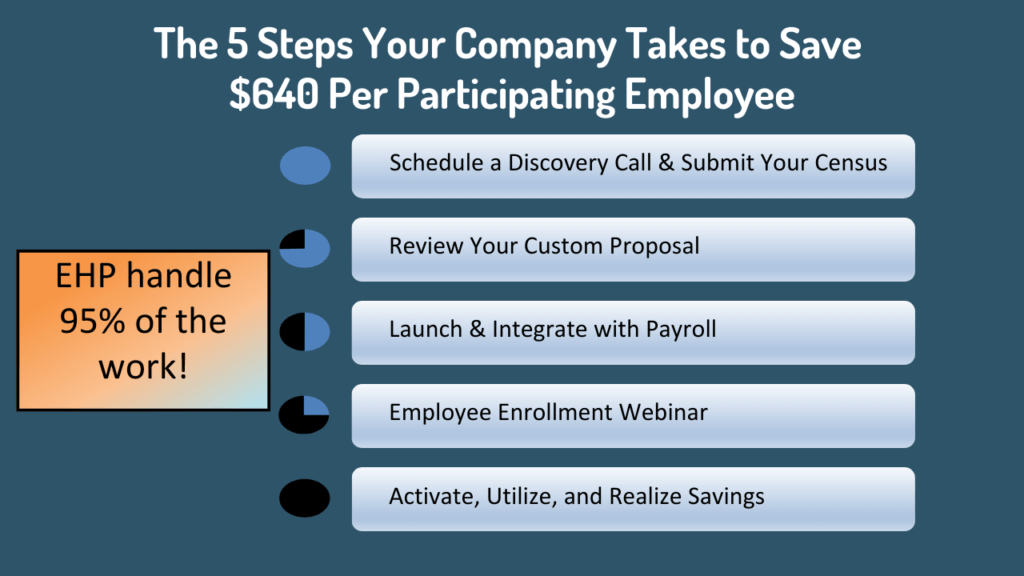

Every dollar you pay in FICA is money that could stay in your business — legally and compliantly. By adding a Section 125 pre-tax deduction (like the one used in programs such as EHP + Revive Health), you lower the taxable wage base for both employee and employer. That creates real FICA savings — often around $640 net per participating employee per year — while funding powerful new benefits at zero net cost to you or your team.

It’s not a loophole; it’s a long-standing IRS-approved strategy that’s finally going mainstream.

Ready to stop overpaying FICA and start turning those tax dollars into better benefits for your team?Schedule a quick discovery call to see how much your company could save.

The Hidden Opportunity Most Owners Miss-

Year after year!